When I was growing up in an outer suburb of London in the 1980s, there was much talk of the decline of the city. In the future, we were told, we would all be working remotely via telescreens from our decentralised living pods.

The economics and technology of the argument seemed solid. The Internet was coming up in earnest (from 1990), and we wouldn’t need to be near each other anymore to do our jobs. In the event, that didn’t happen, and property prices in London rose dramatically as people clustered to where the jobs were in the later 90s, the noughties, and up until 2020.

COVID, of course, has changed all that.

In this article, I want to take a peek into the future and speculate on what will be the medium term effect on London of the systemic shock COVID has brought to our working practices and assumptions.

Here’s the flow of the analysis:

- Working from home is now a thing

- 50% of office space is not needed

- How much office/residential/retail space is there?

- How long will this take?

Skip to ‘Consequences‘ below if you’re not interested in the analysis.

Working From Home Is Definitely Now A Thing

There’s no doubt that WFH is now a proven model for working. Whatever objections existed in the past (and difficulty was had negotiating it) few businesses now think that having everyone in the office all the time is essential or even desirable for their bottom line. Most managers used to furrow their brow if someone wanted to WFH and grudgingly offer it as a ‘perk’, and maybe let them WFH for one day a week. Pre 2020, a few plucky businesses (normally startups or smaller tech firms) offered or embraced remote working, but these were a relatively low proportion of all businesses or workers in the economy.

But right now, many companies are effectively operating as distributed businesses that telecommute. Many reports say that office workers will not return until 2021. And when they do, their habits will have ineradicably altered.

But there’s also no doubt WFH is not for everyone all of the time. Many people want or even need the physical social contact that work gives them. On the other hand, CFOs across the capital must be looking at their operating costs and wondering by what percentage they can be cut.

So the question arises: how much less office space can people use and still be productive and content? Right now I would estimate we are at near 80% of office space going unused in central London (I work alone from an office in Central London at the moment (July 2020), and apart from construction and security workers, it’s eerily quiet here).

I’m going to take a guess here and say that businesses – on average – will be planning to cut 50% of office space. Some people will go back full time, some people will come in for a few days a fortnight, and some will come in rarely (if at all). On the other hand, extra space may be be needed to maintain safety from next year. Fifty percent seems a reasonable estimate. It’s also backed up by anecdotal stories coming from the City:

“If we have learned nothing we have learned that 40-50% of staff

can work from home. For the time being some leases are long

but there should be plenty of room if only 50% of the staff

are present every day, without requiring extra space.”

Source

How Much Office Space Is There?

What does 50% less office space utilisation actually mean for London? How significant is this, historically?

Firstly, I’m going to look at office space in Central London. The best figures I could find were here, from 2012.

| Borough | Square metres | Square feet |

| Westminster | 5,373,000 | 57,800,000 |

| The City | 5,000,000 | 53,800,000 |

| Tower Hamlets | 2,458,000 | 26,400,000 |

| Camden | 2,137,000 | 23,000,000 |

| Islington | 1,455,000 | 15,700,000 |

| Southwark | 1,270,000 | 13,700,000 |

| TOTAL | 17,693,000 | 190,376,680 |

There was 190m sq ft of office space in these central boroughs in 2012. This source suggests that this doesn’t move much every year, (some 800,000 sq feet of space was converted to residential, but new offices are also being built) so if it has moved since, it would be in the low millions. Other sources suggest that the change in office space was roughly +1% per year between 2000 and 2012

So let’s assume we lose the need for around 90-100m sq ft of space. What do these figures mean, in a historical context?

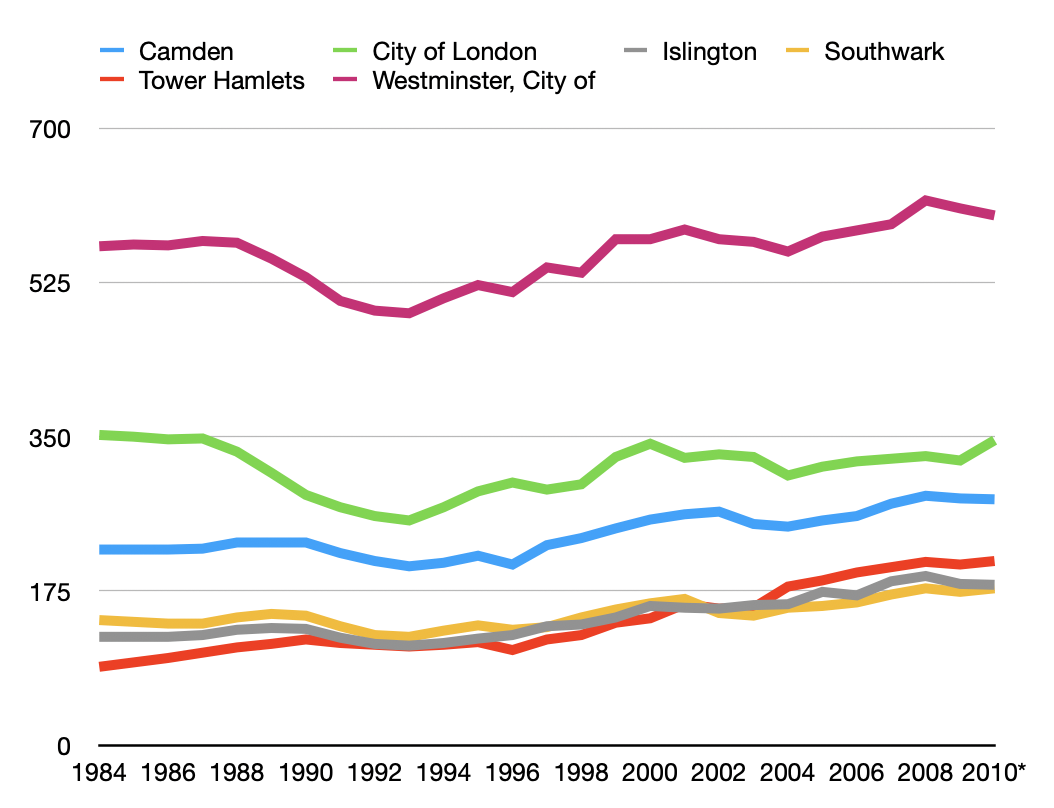

This source tells us the number of jobs per London borough between 1984 and 2010. Usefully, in the middle of this was a large recession which reached its nadir in 1993.

A quick look at the numbers for the City of London tells us that the peak (2010) to trough of jobs (1993) in town was about 20%. So a big recession (the 90s was a pretty big one) resulted in 20% fewer people working in town.

The effect of a 50% reduction is therefore utterly seismic. We’re in uncharted territory.

I don’t know how far you’d have to go back to get back to those levels. Leaving the war aside, maybe the 1950s had similar levels of people working in London then? Before that, you’d have to go back to times when horses were the main means of transport in London, which was effectively a different world.

How Much Household Space Is There?

So if half the office space is no longer needed, can this space be converted into residential property?

To figure this out, we need to know:

- How many Central London households are there?

- How big is the ‘typical’ Central London household?

- How much can be converted at once?

We have the number of households recorded here:

| Borough | Number of Households |

| Westminster | 117,100 |

| The City | 0 (ie negligible) |

| Tower Hamlets | 121,200 |

| Camden | 111,400 |

| Islington | 108,800 |

| Southwark | 128,600 |

| TOTAL | 587,100 |

We have 587,100 households. The median household size (based on a Rightmove search of EC1 + 1 mile) is two bedrooms.

| Bedrooms | Number for sale |

| Studio | 187 |

| 1 | 944 |

| 2 | 1306 |

| 3 | 554 |

| 4 | 77 |

| 5+ | 36 |

The average size of a 2 bed in this area is ~800 square foot, so the estimated floorspace of residential property in Central London is: 587,100 * 800 = 469,680,000 square feet.

So the amount of ‘freed up’ office space (~ 90-100m sq feet) gives about 20% extra residential space to Central London, if it were all to be ‘handed over’ instantaneously.

How Much Retail Space Is There?

London doesn’t just contain office and residential space, there’s also retail. From this source, the figures show that the amount of space is – relatively speaking – not that significant:

| Borough | Square metres | Square feet |

| The City | 2,810,000 | ~3,000,000 |

| Westminster | 1,973,000 | ~21,200,000 |

| Camden | 637,000 | ~6,900,000 |

| Islington | 413,000 | ~4,400,000 |

| Southwark | 434,000 | ~4,700,000 |

| Tower Hamlets | 455,000 | ~4,900,000 |

| TOTAL | 6,722,000 | ~45,000,000 |

Aside from noting its relative lack of size, predicting whether retail floorspace will go up or down is harder to determine. If people move in, retail demand may increase. If people stop working there, it may fall. If floorspace gets cheaper, larger retailers may move back into town to take advantage of Central London’s connectivity to sell more. So I think retail floorspace demand can safely be ignored for the purposes of this discussion.

How Long Will This Take?

If we do indeed need 50% less office space, then how long will this take to work through the system? Obviously, we can’t just wake up tomorrow and start using half of our offices as residential homes, so at least two factors are at play here:

- How long office leases are

- How quickly offices can be converted to residential

How Long Are Commercial Leases?

According to this source, the typical commercial lease length is 3-7 years. If we split the difference to get the average remaining lease time, that’s 5 years. So, if the typical company was halfway through their lease when the pandemic hit in March, that gives us 2.5 years remaining for the average firm. Half a year later, we’re not far off being 2 years away from when the typical lease ends.

So that’s just two years before 25% of Central London office spaces become vacant. This is frighteningly quick.

How Fast Can Offices Be Converted To Residential?

As mentioned above, 800,000 sq feet of office space was converted to residential in 2013. That might be considered a fairly typical year. To convert 90-100m square feet of office space to residential would therefore take about 100 years in ‘normal’ times. This is clearly far too slow.

At least two factors limit this possible rate of change: the speed of the planning system, and the capacity of the building trade to supply skills.

Consequences

Here’s some of the consequences we might speculate will happen as a result of this sudden demand shock.

Expect the price of office space price to plummet

This one’s a no-brainer – if demand for offices drop, expect a fast drop in the price of office space in London. This might mean businesses open up more expansive spaces, maybe with more old-style physical offices or flexible meeting rooms to take advantage.

Expect London wages to fall

As property costs fall, London wages might be expected to fall, as the pool of staff to compete with goes beyond those that need or want to live in London.

Expect pressure on the planning system

One of the first things we’d expect to see is pressure on the planning system to move faster. As offices vacate, many requests for change of use will come in.

City planning systems are not famed for their efficiency or speed, so I don’t expect this to be fast (especially if numbers overwhelm the system). But this source suggests that smaller requests take 8 weeks to process. I’ve no idea how realistic this is, nor do I know how long it takes for the ‘larger, more complex developments’ mentioned.

This source suggests that ‘Since 2013 the conversion of B1/B8 commercial premises to a dwelling house is considered to be a permitted right. It does not therefore require a Change of Use Planning Application.’ I don’t know how many offices this would cover, nor can I shake the suspicion that it can’t be that easy. Maybe a reader can enlighten me?

Expect a boom for builders

Whatever happens, I expect a boom in the building trade in London. Already, many businesses have taken the opportunity in the lull to refit their buildings, and Central London is awash with builders driving, carrying goods, and shouting to each other near my quiet office. The next few years will be boom time in London for anyone running a building firm as cheap labour and high demand.

Expect reduced transport investment

Fewer workers in London means far less strain on the transport system. In recent decades London has invested enormously in transport infrastructure and capacity. I can remember the abysmal state of the Tube and buses in the 80s: hours spent waiting for buses that arrived in batches, and tube trains that ran infrequently. I can even remember the filthy smoking carriages on the underground. But I digress.

This article from 2013 gives some idea of the sums involved and the plans London had. I expect there to be pressure to not only curtail these plans, but also to reduce services more generally as fewer people pressure the system at rush hour.

Expect even more pubs to disappear

The traditional City pub has been under pressure for some years now, but this will take things to a completely new level. A far-sighted historical blogger has already taken pictures of these pubs in preparation for their demise.

Expect property prices in London to fall, and surrounding areas to rise

The effect on residential property prices in Central London itself is difficult to gauge, as I don’t have a ready model. On the one hand, the conversion of just under 100m square feet of office space to residential will increase supply about 20%, as discussed above.

At first glance, this suggests a straightforward fall in property price. How much is unclear, because previous comparisons (eg with the low property prices of the late 90s) coincided with a general and significant recession (ie a sustained fall in economic output). It’s quite possible that we will have a ‘V-shaped recovery’ without people returning to the office. This is, to use an over-used term, unprecedented.

London workers are already fleeing (not just Central) London, and we’re already seeing the signs of this, with analysis flummoxed by an ‘unexpected mini-boom‘ in the surrounding areas:

‘It can’t be denied that lockdown really emphasised the need to move for many, particularly those who were considering upsizing or leaving London for the commuter belt and we expect this to continue, particularly as workers are told they may not be going back into the office until next year.’

Source

Demand for buying the smaller ‘pied a terre’ properties that already abound there may increase significantly, as those fleers decide to retain a convenient bolt-hole in town. This could moderate the fall of (or even raise) the cost for these properties.

Conclusion

Property markets are dynamic systems, so the scenario above is unlikely to play out as straightforwardly as I’ve analysed it. That’s what makes economics fun. So let’s speculate a bit further.

Any significant drop in property values results in a relative rise in value in surrounding areas as people flee the town. This economic boost to previously ‘failing’ areas could play into the Conservative government’s hands as private investment in these areas replaces or works alongside public investment to produce an economic ‘feelgood’ factor.

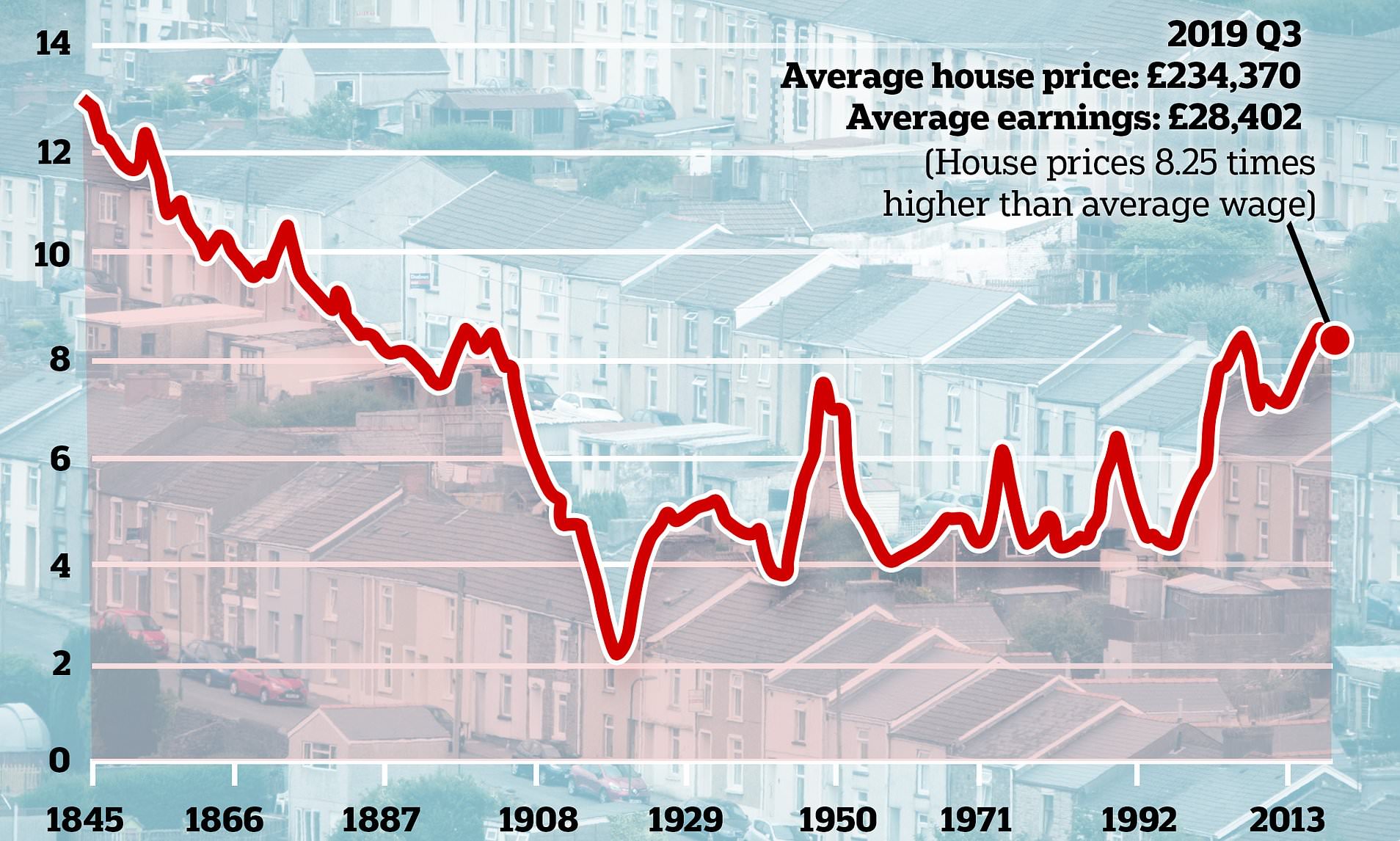

I was tempted to compare the effect of this to wars, but this graph of house prices compared to wages stopped me in my tracks.

You can see that wars appear to have had an effect (drops during the 1910s and the 1940-1945s), but that these pale compared to the steady fall between 1845 and the first world war. According to the analysis, this had three factors: rising incomes, more houses, and smaller houses:

‘The Victorians and Edwardians didn’t just build more houses, they more

than doubled the housing stock in England, Wales and Scotland between

1851 and 1911 – from 3.8 million houses to 8.9 million houses.’

Source

This time we may well have a 20% increase in supply in Central London, and an unknown, but possibly similar, increase in supply in the suburbs that depend on Central London activity. A back of envelope calculation suggests that prices could fall by about a third relative to incomes (which could themselves fall significantly, as noted above). In real terms, therefore, we could see London property prices halve.

And this is in the context of demographics which suggest that real London property prices were already under pressure. This 2005 paper from the Federal Reserve predicted a significant real terms fall in UK house prices going out to 2030, and in the last 15 years hasn’t been that far off the mark.

But it’s important not to forget that there is a significant economic benefit to the innovations that working in physical proximity brings. Cities are where ‘ideas have sex‘, and these ideas have intangible value that translates to economic value that justify the city premium. Looking past the next few years, if London property prices fall then young workers will take advantage of the situation to move back in and generate value however it’s done in the future, acting as a brake on any falls. In the meantime, other UK cities could boom as their relative value and compatibility with this new way of working work to their advantage.

Sources

Mini boom pushes house prices record high says Rightmove – BBC

The quiet grinding loneliness of working from-home – The Guardian

London workers to return to office after Christmas – The London Standard

London needs 13 million square feet of extra office space for bankers to return – FN London

London rail infrastructure investment – FT

Lease term length – tenantbase.com

London City Pubs – alondoninheritance.com

FTSE-100 firms stay-at-home plans – The London Standard

https://www.statista.com/statistics/1042514/office-space-in-london-areas-by-sector/

The London Plan, first published 2004

London commercial and industrial floorspace by borough – data.london.gov.uk

Housing tenure by borough – data.london.gov.uk

Historical London jobs by borough and industry – data.london.gov.uk

If you enjoyed this, then please consider buying me a coffee to encourage me to do more.